You only pay when you win. When Chargeback Shield wins a dispute for you, it keeps 18% of

the recovered amount (10% on Business). That fee is added to your regular monthly statement —

it’s never pulled from your wallet or your payout. Lose a case and you pay nothing; there’s no

monthly subscription, and letting a small dispute go is always free.

/security/disputes). The first time you open it — before any dispute has come in — it

introduces itself: what it does, what it costs, and where to configure it.

How it works

A chargeback (also called a dispute) is filed against the gateway that processed the payment — Stripe disputes live in Stripe, PayPal disputes live in PayPal. Shoppex receives the notification, surfaces it here, and goes to work automatically.1

A buyer charges back

The dispute shows up here the moment it happens, straight from your Stripe or PayPal

account. There’s nothing to install and nowhere else to watch — Shoppex already has the

connection.

2

We build your defense

Chargeback Shield assembles an evidence packet from data only you have: the download

log proving the buyer received the file, license activations from the buyer’s device, and

the buyer’s prior order history. Generic dispute tools can’t see any of this — your

storefront produced it.

3

We submit it before the deadline

The packet is sent to the bank inside the gateway’s evidence window. You can approve every

case yourself, or let it run fully automatically. Win, and the money comes back to you.

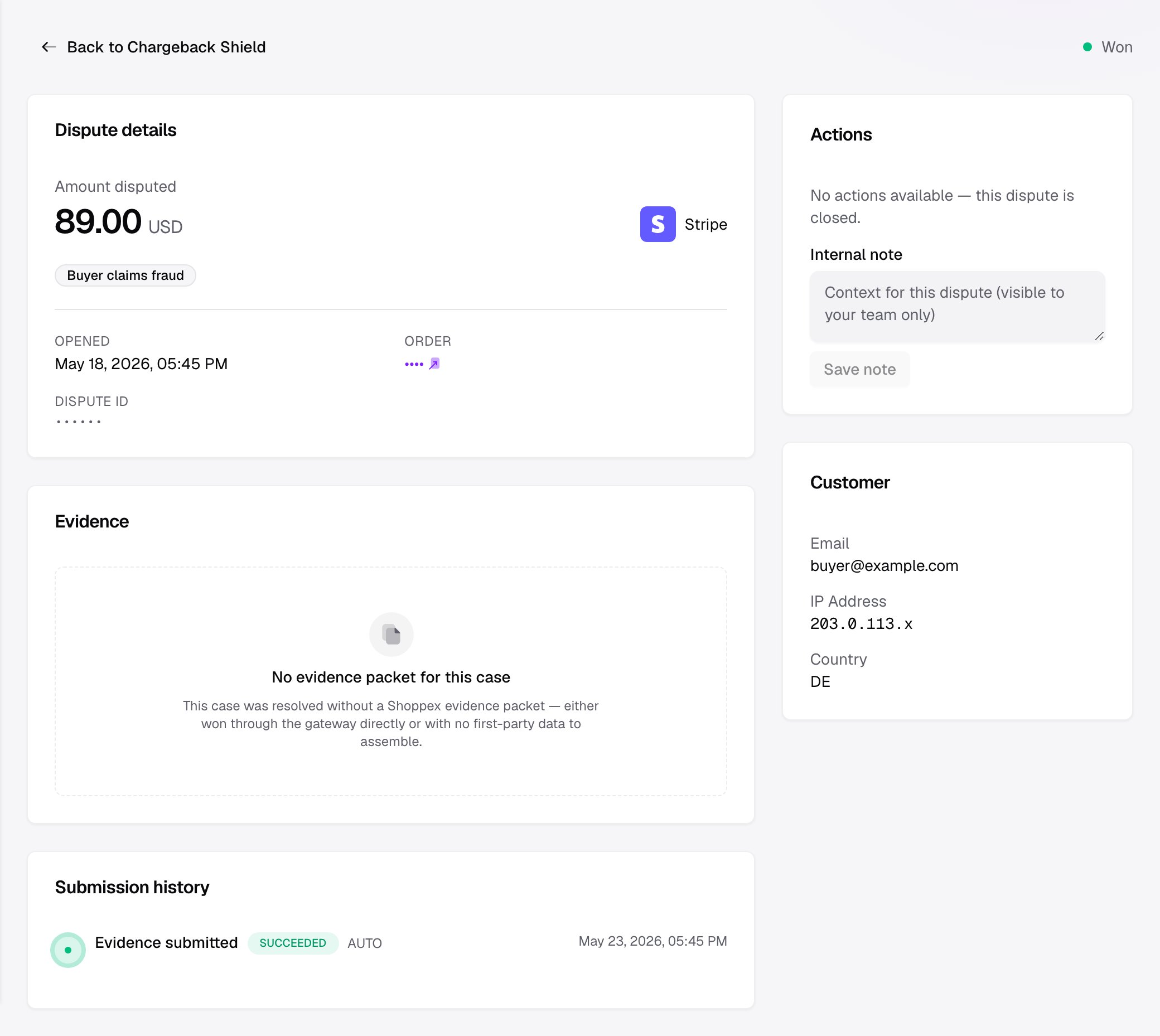

Chargeback Shield never invents evidence. Every item in a packet is real telemetry your

store recorded — a delivery event, a license ping, a past paid order. If the data needed to

defend a case isn’t there, the case is flagged for your review instead of being submitted

with a weak packet.

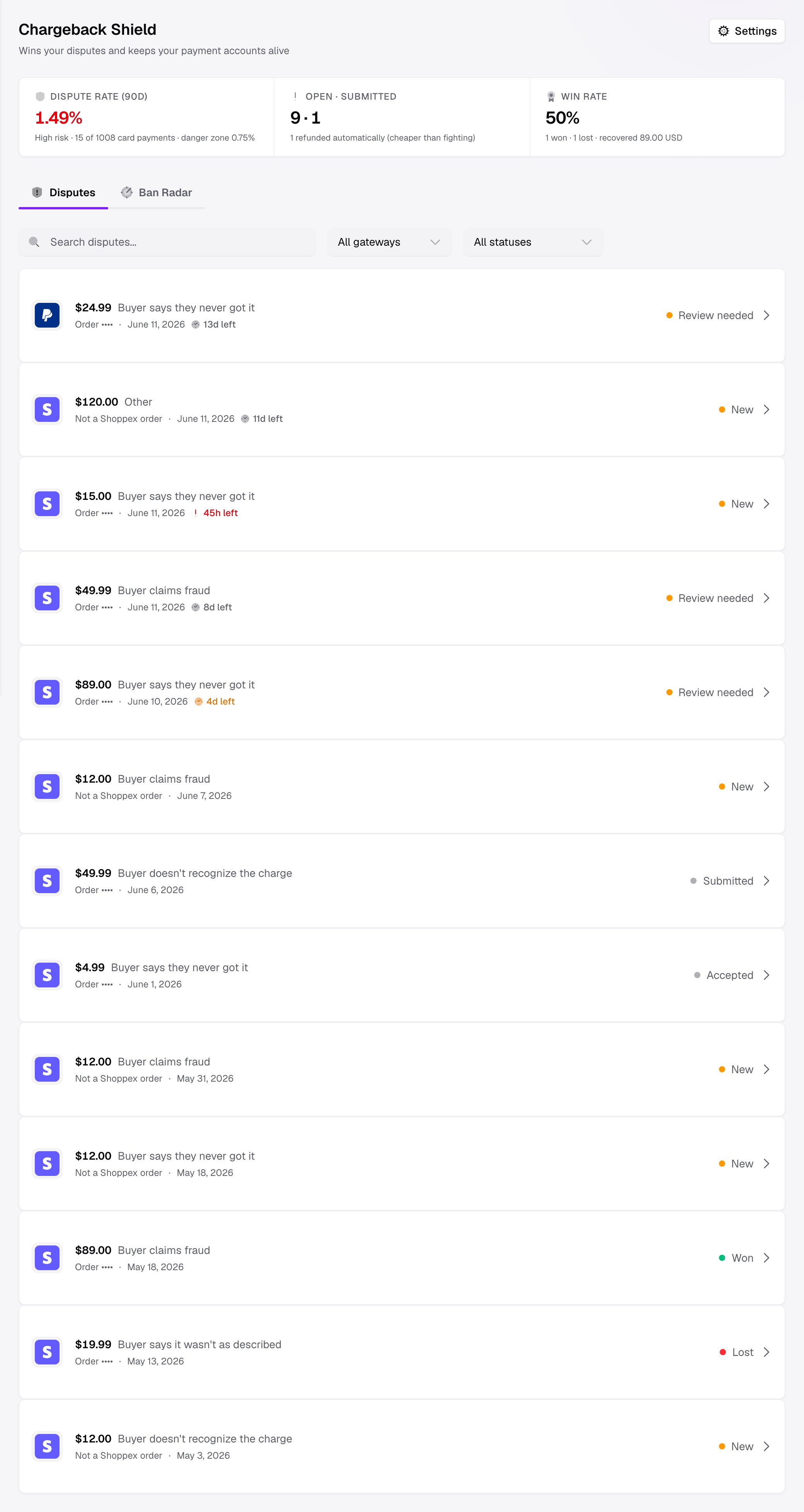

The Disputes view

The Disputes tab is the working surface. A health strip across the top answers the question merchants actually care about — is my account safe? — followed by every dispute and its current state.

- Dispute rate (90d) — your rate over the last 90 days, coloured Healthy, At risk, or High risk against the zone where processors start watching. This is the headline because account survival, not recovery, is what costs sellers their business.

- Open · submitted — how many cases are still in flight versus already sent to the bank.

- Win rate — how many you’ve won and lost, and how much money has been recovered.

A single case

Opening a dispute shows everything Chargeback Shield knows about it: the amount and reason, the evidence packet it assembled, the submission history, and the customer details captured at checkout.

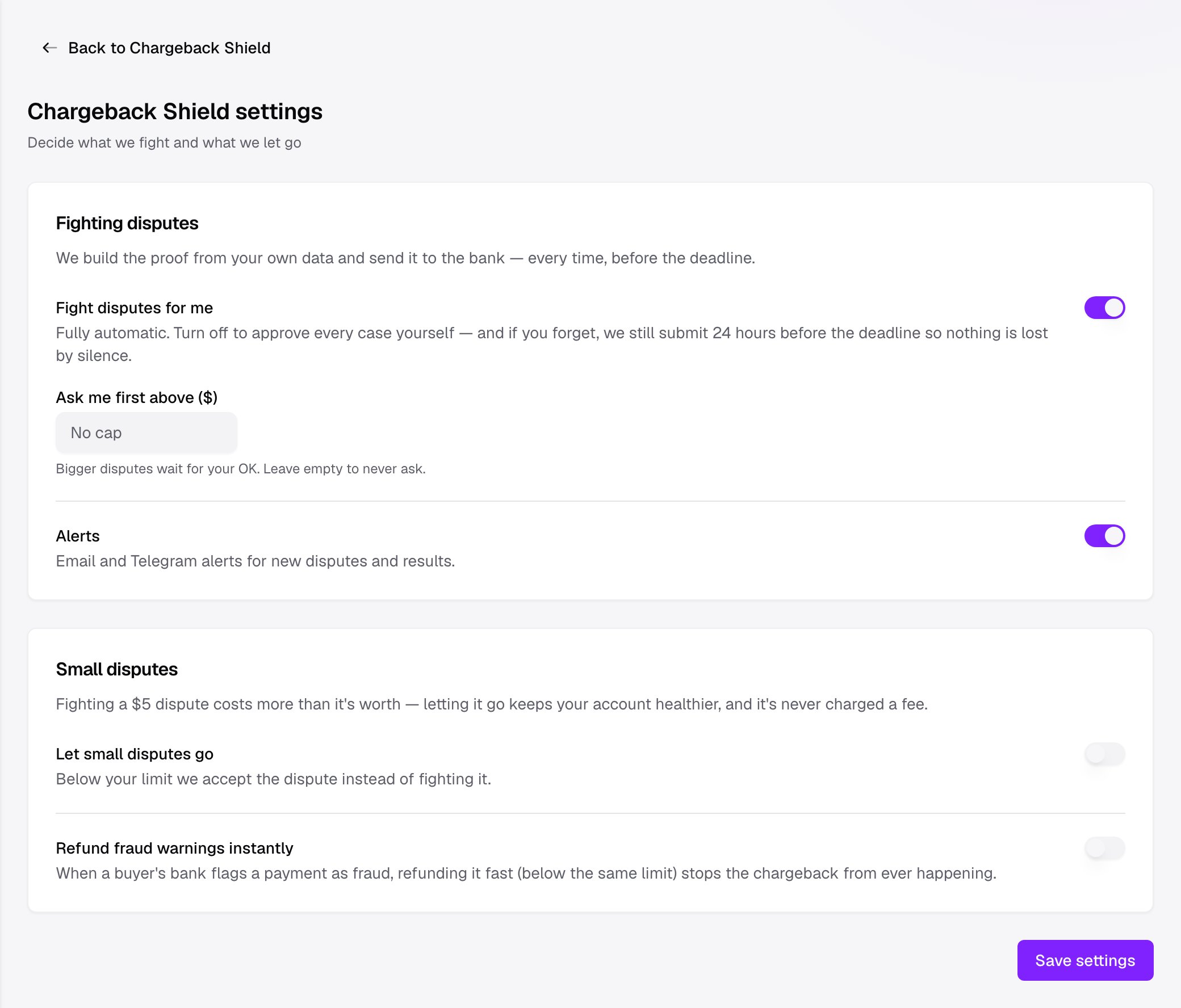

Settings — what to fight and what to let go

Open Settings from the Chargeback Shield header to decide how much Chargeback Shield does on its own.

Fight disputes for me

Fight disputes for me

Fully automatic submission. Turn it off to approve every case yourself — and if you forget,

Chargeback Shield still submits 24 hours before the deadline, so nothing is ever lost to

silence.

Ask me first above ($)

Ask me first above ($)

When automatic fighting is on, set a value here to hold the biggest disputes for your

approval. Smaller ones are handled for you; anything above the amount waits for your OK.

Leave it empty to never be asked.

Let small disputes go

Let small disputes go

Fighting a $5 dispute costs more than it’s worth, and accepting it keeps your account

healthier. Below the limit you set, Chargeback Shield accepts the dispute instead of

fighting it — and accepting is never charged a fee.

Refund fraud warnings instantly

Refund fraud warnings instantly

When a buyer’s bank flags a payment as fraud before a dispute is filed, refunding it

quickly (below the same small-dispute limit) stops the chargeback from ever happening.

Alerts

Alerts

Email and Telegram alerts for new disputes and their results, so you’re never surprised by

an outcome.

What it costs

Chargeback Shield is success-based — there’s no monthly subscription and nothing to pay up front.- A fee applies only on disputes it wins for you. When the autopilot submits your evidence and the case is won, Chargeback Shield keeps 18% of the recovered amount (10% on Business).

- The fee goes on your monthly statement. It’s billed alongside your other platform fees at the end of the month — never deducted from your wallet or held back from a payout.

- You’re never charged for a loss, an accept, or a case you handled yourself. Lost disputes, small disputes you let go, and disputes you won directly in Stripe or PayPal carry no fee.

Because the fee only ever comes out of money Chargeback Shield recovers, turning it on can’t

leave you worse off than ignoring a dispute would.

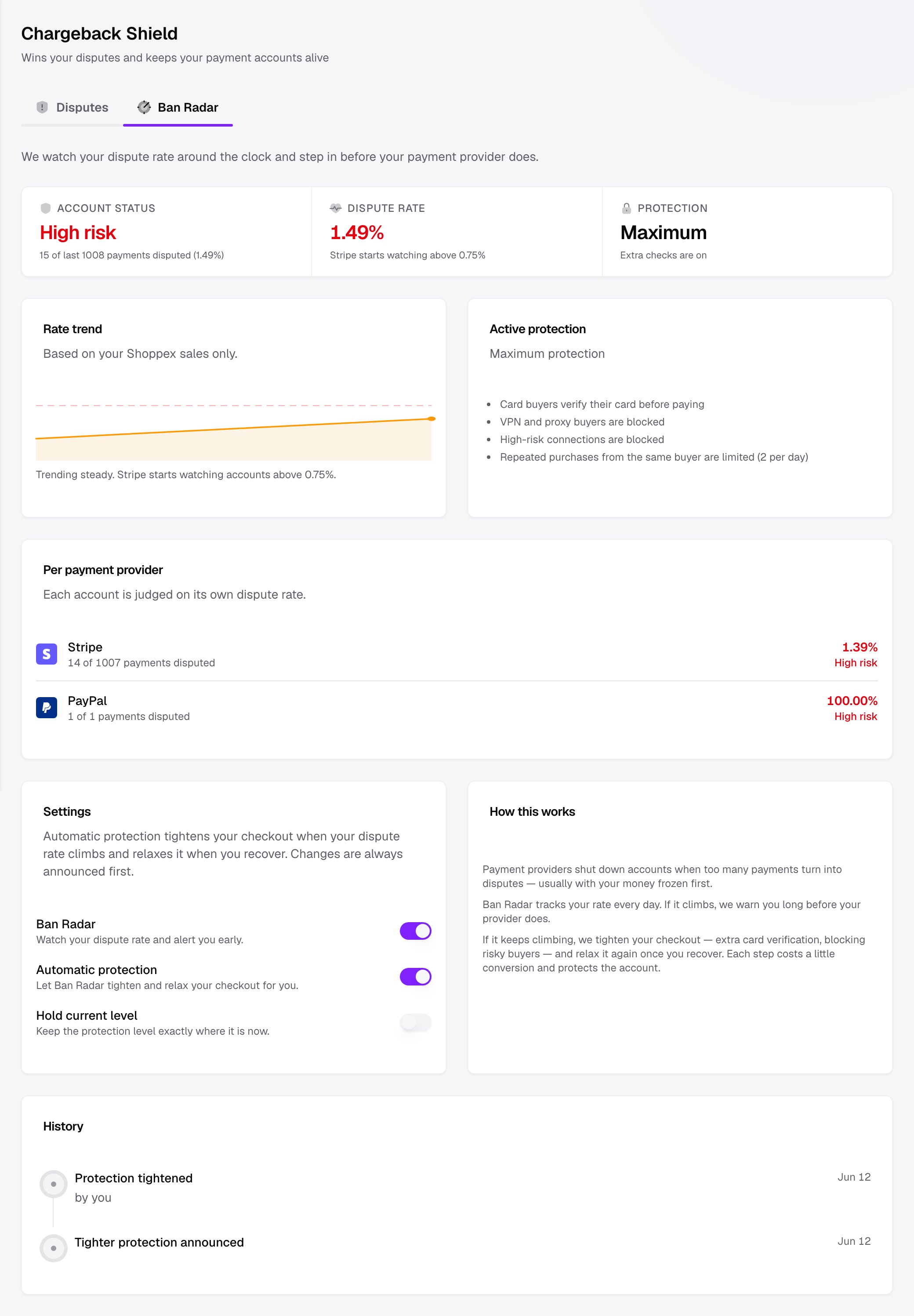

Ban Radar — keeping your account alive

Winning disputes is only half the job. The other half is keeping your dispute rate out of the zone where Stripe and PayPal freeze your money and close your account. That’s Ban Radar, the second tab inside Chargeback Shield (/security/ban-radar).

- Account status — Healthy, At risk, or High risk, with the number of disputed payments behind it.

- Dispute rate — your current rate, next to the point where Stripe starts watching accounts.

- Protection — whether extra checkout protection is currently Normal, Protected, or at Maximum.

Automatic protection

When your rate climbs, Ban Radar can tighten your checkout to bring it back down, then relax it again once you recover. The protection it applies is a runtime layer on top of checkout — it never changes your saved settings:- Card buyers verify their card before paying (3-D Secure)

- VPN and proxy buyers are blocked

- High-risk connections are blocked

- Repeated purchases from the same buyer are limited

You’re always warned first. The very first time Ban Radar tightens your checkout it

announces the change ahead of time — you can apply it immediately, dismiss it, or hold your

protection level exactly where it is. Each step costs a little conversion and protects the

account; the choice stays yours.

What Chargeback Shield is good for

Digital-goods sellers

Most disputes on digital goods are “I never got it” or “I don’t recognise this charge.”

Your download logs and license activations answer both — automatically.

Sellers who don't want to babysit disputes

Turn on automatic fighting and Chargeback Shield handles the whole lifecycle: assemble,

submit, follow up, and let small ones go.

Anyone on Stripe or PayPal

Ban Radar keeps your dispute rate out of the account-closing zone, so one bad week doesn’t

cost you your payment provider.

Stores that want their money back

Evidence built from your own data wins cases generic tools can’t — and you only pay when it

works.